Asia-Pacific PCB Assembly Market to Reach USD 58.2 Billion by 2033 Amid EV Expansion and AI Infrastructure Investments

The Asia-Pacific PCB Assembly Market is projected to grow from USD 31.9 billion in 2025 to USD 58.2 billion by 2033, registering a CAGR of 7.8% during the forecast period. The market is benefiting from rising electronics manufacturing activity across China, Taiwan, South Korea, Japan, India, and Vietnam, as well as increasing demand for high-performance printed circuit board assemblies used in electric vehicles, AI servers, telecommunications equipment, and industrial automation systems.

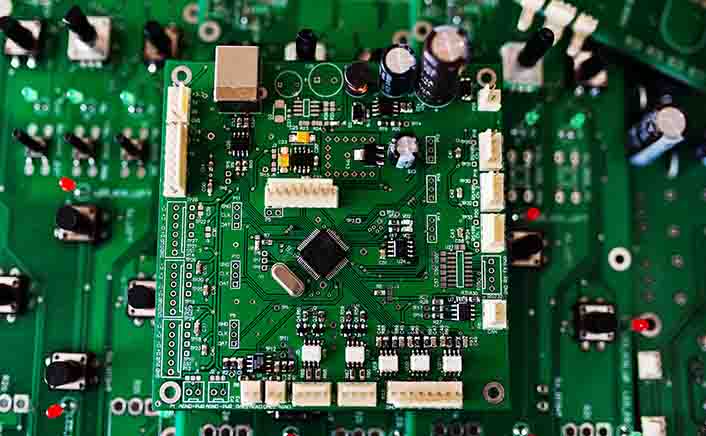

PCB assembly forms the operational backbone of modern electronic devices by integrating semiconductor components onto printed circuit boards through technologies such as Surface Mount Technology (SMT) and through-hole assembly. Asia-Pacific continues to dominate global PCB assembly capacity due to its large-scale electronics manufacturing ecosystem, established supplier networks, semiconductor integration capabilities, and cost-efficient contract manufacturing infrastructure.

The rapid expansion of electric-vehicle manufacturing is becoming one of the strongest drivers of PCB assembly demand across the region. Electric vehicles require substantially higher PCB content than traditional vehicles because of battery management systems, advanced driver assistance systems (ADAS), infotainment modules, onboard charging systems, and power electronics integration. China alone produced more than 9 million electric vehicles in 2024, creating significant demand for multilayer and high-density PCB assemblies capable of handling complex automotive electronics applications.

The growing deployment of AI computing infrastructure is also transforming the market landscape. AI servers and hyperscale data center systems require advanced multilayer and High-Density Interconnect (HDI) PCBs that support high-speed data transmission, thermal management, and compact system architectures. Taiwanese electronics manufacturers supplying AI server platforms to global cloud and semiconductor companies are expanding investments in precision PCB assembly capabilities to meet rising demand from AI-driven computing applications.

Telecommunications infrastructure development across the Asia-Pacific is further strengthening market expansion. Countries including China, South Korea, and Japan continue to accelerate 5G network deployments, increasing demand for networking hardware, telecom base stations, and high-frequency communication systems that require advanced PCB assemblies. Telecom equipment manufacturers are increasingly adopting automated SMT assembly lines and AI-enabled inspection systems to improve production accuracy and reduce manufacturing defects in complex communication hardware.

Supply-chain diversification strategies are also reshaping regional PCB assembly investments. Global electronics companies are gradually expanding manufacturing operations beyond China into emerging production hubs such as India and Vietnam. India’s Production Linked Incentive (PLI) scheme and electronics manufacturing incentives have accelerated investment in smartphone and electronics assembly by multinational manufacturers and EMS providers. Vietnam has similarly strengthened its position as a key destination for electronics exports, driven by competitive manufacturing costs and rising foreign direct investment in electronics production.

Technological evolution within the PCB assembly industry is increasingly centered on automation and miniaturization. Surface Mount Technology remains the dominant assembly method due to its ability to support compact PCB designs and high-volume automated production. Manufacturers are integrating advanced optical inspection systems, automated soldering platforms, and AI-driven defect-detection technologies to improve assembly precision in automotive, aerospace, telecom, and industrial electronics applications.

Despite strong market fundamentals, the industry continues to face several operational challenges. Semiconductor supply fluctuations, geopolitical trade tensions, and rising environmental compliance costs remain significant concerns for PCB assembly providers. The market also faces pricing pressure due to intense competition among high-volume contract manufacturers operating across China and Southeast Asia. In addition, the increasing complexity of PCBs associated with AI hardware, autonomous vehicles, and next-generation telecom systems is forcing manufacturers to invest heavily in advanced assembly equipment and skilled engineering capabilities.

Consumer electronics currently account for the largest share of PCB assembly demand across Asia-Pacific due to the region’s dominance in smartphone, laptop, wearable device, and home electronics manufacturing. However, automotive electronics is expected to emerge as one of the fastest-growing application segments over the forecast period as EV adoption and connected vehicle technologies continue to expand across regional markets.

Major companies operating in the Asia-Pacific PCB assembly market include Foxconn, Pegatron, Wistron, Jabil, Flex, and TTM Technologies. These companies are prioritizing investments in automation, regional expansion, and advanced PCB assembly capabilities to strengthen their competitive positioning in the evolving electronics manufacturing ecosystem.