U.S. Co-Packaged Optics Market to Reach USD 466 Million by 2033, Driven by AI Infrastructure Expansion and Silicon Photonics Innovation

The U.S. Co-Packaged Optics Market is projected to grow from USD 50 million in 2025 to USD 466 million by 2033, registering a CAGR of 31.8% during the forecast period. Market growth is being fueled by rising investments in artificial intelligence (AI) infrastructure, the increasing deployment of high-performance computing (HPC) clusters, the rapid expansion of hyperscale data centers, and the commercialization of silicon photonics technologies designed to overcome the power and bandwidth limitations of conventional networking solutions.

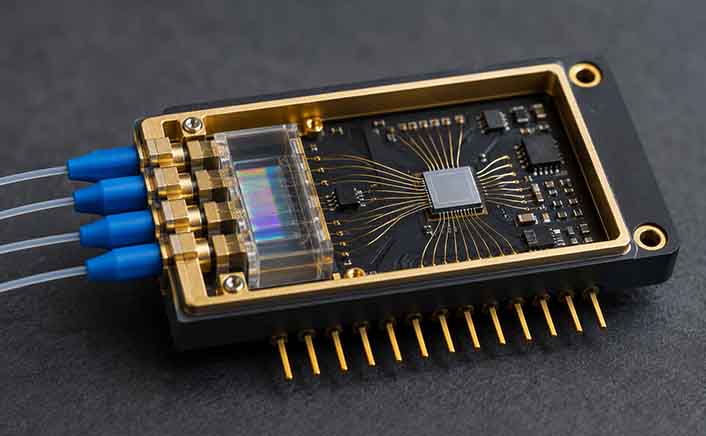

Co-packaged optics (CPO) is emerging as a critical technology for next-generation data centers by integrating optical engines directly with switching silicon. This architecture minimizes electrical signal loss, reduces power consumption, increases bandwidth density, and improves overall system efficiency. As AI training and inference workloads generate unprecedented data traffic, hyperscale cloud providers and semiconductor companies are accelerating the adoption of CPO to support future networking requirements.

The United States remains at the forefront of CPO innovation due to its advanced semiconductor ecosystem, strong silicon photonics research capabilities, and concentration of leading cloud service providers and networking equipment manufacturers. Federal initiatives supporting semiconductor manufacturing, advanced packaging, and domestic technology leadership are further strengthening the country's competitive position.

Data center networking represents the largest application segment, driven by the growing need for high-speed interconnects that connect thousands of GPUs and AI accelerators within large-scale computing clusters. Traditional pluggable optics increasingly struggle with bandwidth scalability, signal integrity, and energy efficiency, making co-packaged optics an attractive alternative for next-generation 800G, 1.6T, and future networking platforms.

AI infrastructure is the primary growth driver. Large language models, generative AI, enterprise AI deployments, and scientific computing require massive data movement between processors, creating demand for networking solutions that deliver higher throughput with lower energy consumption. Co-packaged optics enable operators to improve performance while reducing operational costs, making it a strategic investment for hyperscale and enterprise data centers.

Advancements in silicon photonics continue to accelerate commercialization. Innovations in photonic integrated circuits, heterogeneous integration, optical engines, and advanced packaging technologies are improving system performance while reducing manufacturing complexity. As production scales and manufacturing processes mature, declining costs are expected to support broader market adoption beyond early hyperscale deployments.

In volume terms, the U.S. Co-Packaged Optics Market recorded approximately 13,500 CPO-enabled networking system shipments in 2025 and is projected to reach 151,000 shipments by 2033. Shipment growth will be supported by expanding AI data centers, increasing cloud infrastructure investments, and the migration toward ultra-high-speed networking architectures.

The competitive landscape is evolving rapidly as companies integrate silicon photonics, optical engines, switch silicon, and advanced packaging into unified networking platforms. Strategic partnerships, acquisitions, and joint development initiatives are becoming increasingly common as vendors seek to accelerate innovation and strengthen their presence in the emerging AI networking ecosystem.

The market is also benefiting from broader investments in U.S. semiconductor manufacturing, advanced packaging facilities, and photonics research. These initiatives are strengthening domestic supply chains while supporting commercialization of next-generation optical networking technologies.

Despite its strong outlook, the market faces several challenges. Co-packaged optics require sophisticated manufacturing capabilities, advanced packaging expertise, and complex thermal management solutions to ensure reliable operation alongside high-performance switching silicon. In addition, evolving interoperability standards and limited large-scale commercial deployment continue to create adoption barriers for some organizations.

Nevertheless, long-term market fundamentals remain highly favorable. Growing pressure to improve data center efficiency, eliminate networking bottlenecks, reduce energy consumption, and support increasingly complex AI workloads is expected to sustain investment throughout the forecast period. As networking becomes a key determinant of AI performance, demand for scalable, high-bandwidth optical interconnect technologies will continue to accelerate.

Leading companies operating in the U.S. Co-Packaged Optics Market include Broadcom, Marvell Technology, NVIDIA, Cisco Systems, Coherent, and Lumentum Holdings. These companies are investing in silicon photonics, optical engine development, AI networking platforms, advanced packaging technologies, and strategic collaborations to strengthen their competitive positions.

The U.S. Co-Packaged Optics Market is expected to maintain robust momentum through 2033 as AI infrastructure investments reshape cloud computing, high-performance computing, and digital infrastructure. Continued hyperscale data center expansion and the growing need for energy-efficient, ultra-high-bandwidth networking solutions will position co-packaged optics as a foundational technology for the next generation of AI-driven computing ecosystems.